When the Goalposts Shift

July 2026

Recent Observations on Russell Indexes, Especially in Small/Micro-Cap Value

An Unusual Year Created an Unusual Benchmark

Spoiler alert: to the disappointment of many of you, we are not discussing soccer today; however, the analogy in our headline is a timely one for investors. Each year, on the fourth Friday in June, FTSE Russell reconstitutes its U.S. equity indexes. For many investors, and in most years, this is not exactly calendar-circling material. For managers of small- and micro-cap strategies, especially uncommon folks like us who truly focus on the smallest end of the U.S. equity universe, Russell reconstitution can lead to some interesting dynamics.

At Pacific Ridge, and going back decades to predecessor firms, our team has always been comfortable looking different from our benchmarks. We invest in the smallest, least efficient portions of the U.S. equity market, where many investors cannot or will not spend their time. As a result, most small- and micro-cap managers tend to invest in companies with market capitalizations well above their benchmarks’ averages. We invest in companies that generate solid cash flow and are selling at attractive valuations. We do not attempt to mimic benchmark size, style and sector characteristics. Those are outputs of our bottom-up process, not inputs.

By the end of the 12 months leading into this year’s June reconstitution, the benchmarks looked increasingly different from the universe of stocks in which we invest. The effects were especially pronounced in the Russell Microcap Value Index, where the benchmark’s size, profitability, and valuation profile had become unusually disconnected from our strategy. They also affected Small Cap Value because our strategy’s weighted average market capitalization is well below that of the Russell 2000 Value Index. Those differences affected relative performance over much of the past year and intensified during the most recent quarter.

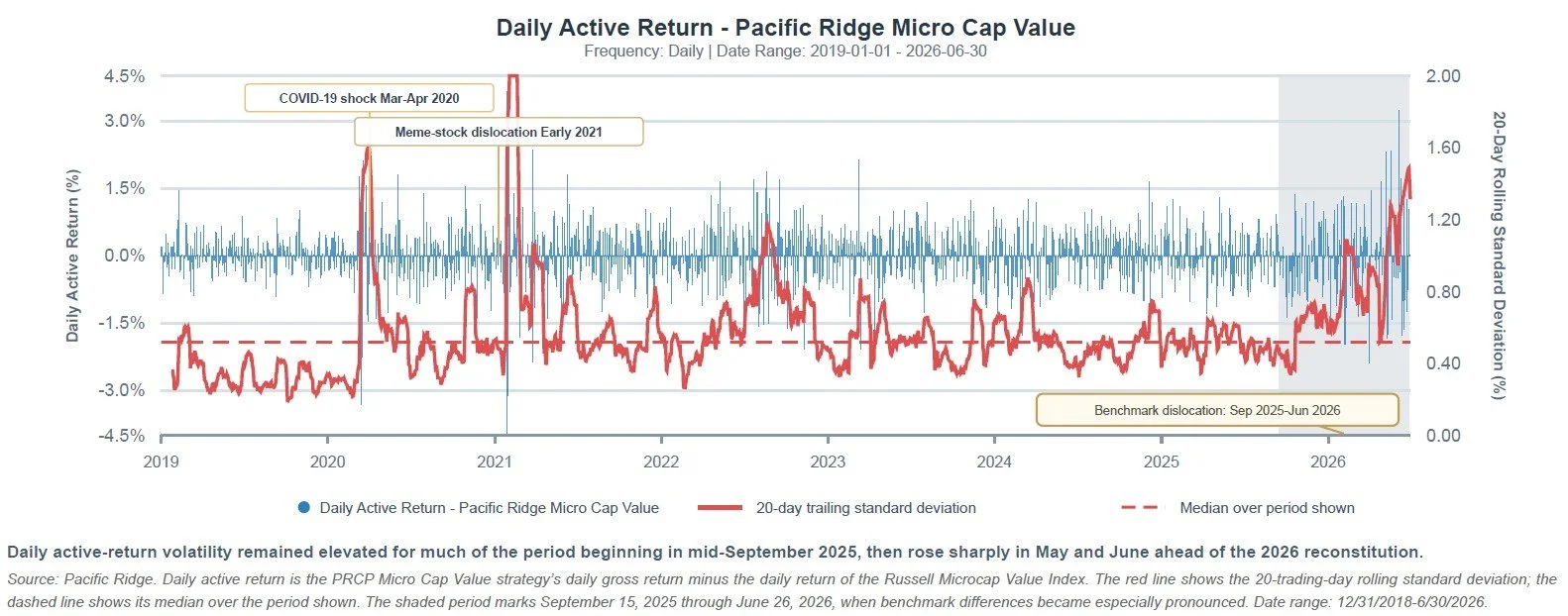

As the chart below illustrates, daily active-return swings were unusually large at times, while the 20-trading-day rolling standard deviation remained above its median for an extended period. The 20-trading-day measure eventually reached levels comparable with the early 2020 pandemic and 2021 meme-stock episodes, after rising particularly sharply in May and June ahead of the reconstitution. The more unusual feature, however, was not simply the peak but the persistence. Some of the volatility reflected broad market forces, including the Middle East conflict and shifting views on AI and data centers. But in our view, the larger issue was the benchmark’s unusual exposure to stocks and themes outside our cash-flow-oriented definition of value.

None of this is to suggest Russell did anything “wrong.” Russell indexes are rules-based, transparent benchmarks. Russell’s growth/value methodology weights book-to-price at 50% and I/B/E/S analyst-estimated medium-term growth and five-year historical sales-per-share growth at 25% each. Those are practical inputs for building an index, but they can become less informative among the smallest companies.

Book-to-price is simply the inverse of the more familiar price-to-book ratio. A company that raised equity, especially at a high valuation, may retain substantial cash even after its share price falls. It can therefore appear relatively “cheap” on book-to-price while still losing money and burning cash. That dynamic can be especially relevant for micro-cap biotechnology companies and helps explain why biotechnology stocks have at times carried such a large weight in the Russell Microcap Value Index. As cash is consumed and book value declines, however, a company can become less value-like under Russell’s methodology and migrate toward growth.

The growth inputs pose a different problem. Many small- and micro-cap companies have limited analyst coverage, while others have short or inconsistent revenue histories. In those cases, Russell’s methodology uses industry-based substitutions or blends company-specific data with industry data, depending on analyst coverage and data availability. That is a practical rules-based solution, but it also highlights the gap between index construction and our work as fundamental investors. We are not trying to classify a company based on incomplete or substituted style inputs; we are determining whether the company can generate durable cash flow and whether the current valuation gives us an attractive return opportunity.

What Changed at Reconstitution

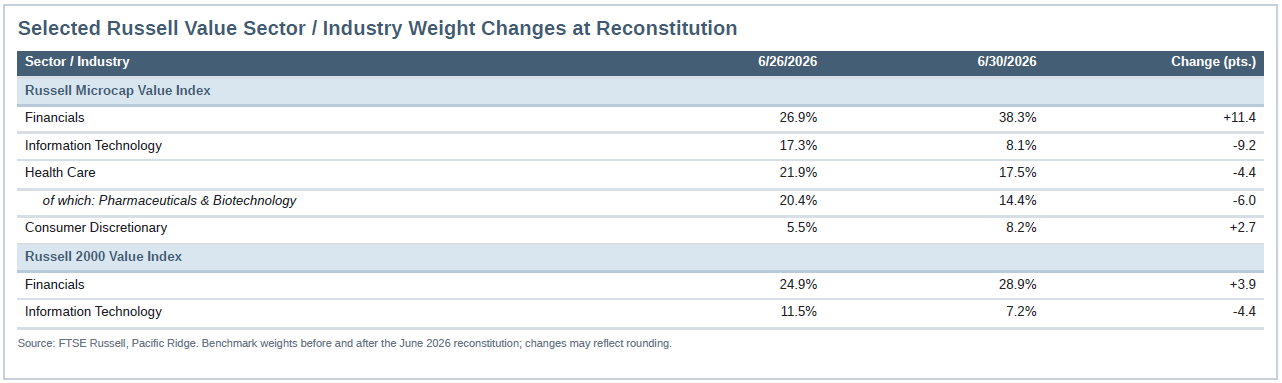

This year’s reconstitution made that drift visible in sector composition. In the Russell Microcap Value Index, Financials increased from 26.9% of the index to 38.3%. Information Technology fell from 17.3% to 8.1%. Health Care declined as well, with the Pharmaceuticals & Biotechnology industry falling from 20.4% of the index to 14.4%. Consumer Discretionary increased from 5.5% to 8.2%. The Russell 2000 Value Index saw similar, though less extreme, shifts.

This is more than just a sector story. Valuation moved meaningfully as well. One simple way to see this is by looking at the total enterprise value to sales multiple of the Russell Microcap Value Index, excluding Financials, where sales-based valuation multiples are not meaningful, and Biotechnology, where most companies have limited or no revenue. The pattern is consistent with what we expected. The index began at a relatively normal valuation after the 2025 reconstitution, became much more expensive over the following year, and reset lower at the 2026 reconstitution.

This is an important reminder that index membership and index weights can change meaningfully after a period of unusually strong performance in stocks that have moved far from their prior size or valuation characteristics. For disciplined, long-term-minded investors like Pacific Ridge, this can make short-term comparisons unusually noisy. Our process did not change. The benchmark did.

We wrote in our November 2025 commentary about what we viewed as a “low quality” rally within small- and micro-cap value benchmarks. That rally continued, with fits and starts, into 2026. Much of the strongest performance came from companies outside our normal definition of value: companies with limited revenue, weak or negative profitability, speculative business models, or valuations that were difficult for us to justify based on cash flow.

Recent Performance and Go-Forward Impact

Both of our strategies generated strong absolute returns in the second quarter. Small Cap Value outperformed its benchmark, while Micro Cap Value trailed a very strong Russell Microcap Value Index. Our quarterly strategy reports, including full performance and our typical attribution analysis, will be out shortly. But given the magnitude of the benchmark reset, we wanted to address the issue directly here.

While we do not want to overstate any short-term performance period, favorable or unfavorable, the attribution provides useful context. In Micro Cap Value, the relative shortfall was concentrated in parts of the benchmark we are structurally least likely to own: larger companies, unprofitable companies, and companies trading at valuations we do not view as supported by normalized cash flow. That mismatch has also been a recurring issue over much of the past year. Measured against the smaller, profitable, cash-flow-generative companies trading at attractive valuations that we target, we are comfortable with how the strategy performed.

There is also a frustrating element to this dynamic. Stocks that helped drive the benchmark higher over the past year, and that we did not own because they did not fit our process, have now either had their weights reduced or left the benchmark entirely. If those stocks later normalize and underperform, the strategy will not receive the corresponding relative-performance benefit from having avoided them. We have seen a version of this movie before. In 2021, by our calculation, simply not owning GameStop cost our Micro Cap Value strategy more than 400 basis points of relative performance during the first half of the year. The stock was then removed from the benchmark after graduating to mid-cap status, and its share price later fell. This time, the issue is broader than a handful of meme stocks, or one particularly large one, but the benchmark math is similar.

What Does and Does Not Change

Beginning in 2026, Russell is moving from one annual reconstitution to two each year, with an additional event taking effect after the close of the second Friday in December. We view that as a sensible change. The December reconstitution will refresh size membership, but it will not fully reconstitute the Growth and Value indexes. Except for additions, deletions, and companies moving into a different size index, existing constituents will retain their June allocations between Growth and Value until the next June reconstitution. The additional size reset should therefore reduce drift, but it will not eliminate the difference between Russell’s definition of value and ours.

The index changes do not alter the broader opportunity we see in smaller companies. As we wrote in our April 2025 commentary, broad valuation disconnects between larger and smaller companies remain meaningful, much like they did coming out of the dot-com period. We do not know when that gap will close. We never do. But the recent market environment has created a number of opportunities beneath the surface. Some stocks tied to AI, semiconductors, semiconductor equipment, and data-center spending have rapidly moved from overlooked to fully valued or overvalued. At the same time, companies in software, consulting, and other areas perceived as vulnerable to AI disruption have been sold off too indiscriminately, in our view.

Our process is not built around predicting index changes, chasing themes, or owning what has recently worked simply because the benchmark owns more of it. We continue to spend our time looking for misunderstood and unloved smaller companies trading at attractive valuations, with balance sheets and cash flow potential that we believe can support strong long-term returns. That opportunity set has pushed our portfolio turnover up a bit, as we take advantage of what the market is handing us.

Benchmarks are useful reference points, and we understand why investors use them. But they are not investment philosophies. By late June, the benchmark had moved far away from the stocks and characteristics we own—in effect, the goalposts had shifted. When that happens, we pay attention. We just do not let it dictate what we buy.

As always, we welcome your questions and look forward to continuing the conversation, perhaps after the World Cup concludes!

Pacific Ridge Capital Partners