Market Commentary

Throughout history, we have observed that major centers of economic power are not static, but instead shift policy slowly over the course of centuries. More noticeable changes may happen in as little as a generation that end up reversing course. We have certainly seen evidence of this over the past few decades with the People’s Republic of China. Following the death of Mao Zedong in 1976, the country slowly opened its economy to the world under the leadership of Deng Xiaoping, adopting free market measures that helped fuel rapid economic expansion following the failed Great Leap Forward and the Chinese Cultural Revolution. While there remained some semblance of state control over certain industries, this “capitalism with Chinese characteristics” dramatically improved living standards for most Chinese citizens.

This trend continued with China’s admission to the World Trade Organization in 2001. The abundance of low-cost labor gradually led to the country being known as the world’s factory. Over the last forty years, over 700 million rural residents were lifted out of poverty as the economy experienced mass industrialization. Along the way, China has become more interconnected with other global powers despite increased wariness as to how the Chinese Communist Party (CCP) might exploit their newfound economic might.

The critical role that China plays in the global economy has become especially apparent in the past few years following the COVID-19 outbreak and supply chain disruptions. As a politically communist country, CCP leadership can take quick decisive action when a crisis emerges. However, this becomes difficult to sustain when forced to make decisions that might be unpopular with its citizenry and risks destabilizing the party’s political control.

For example, take the efforts by economic planners to curtail the level of debt in their overleveraged economy, a looming crisis that has dogged the country for years. When previous efforts threatened to slow the economy, the government quickly reversed course to maintain sufficient growth. Much of this debt is tied in real estate, the main avenue for savings and wealth creation for China’s burgeoning middle class. This became especially apparent in the past few weeks as Evergrande, a major real estate developer, missed its bond payments. With $300 billion in debt outstanding and a critical role in a segment that represents 25% of China’s GDP, the implications of Evergrande’s insolvency are significant.

While the Chinese government is heavily involved in efforts to cushion the blow to their economy, there is a high risk of a domino effect on derivative impacts from the collapse of Evergrande. Many other real estate developers are dependent on liquidity from capital markets. A crisis of confidence could quickly spiral out of control with consumer demand for new housing units. Contagion to industry suppliers could transition into a broader liquidity squeeze that would ripple through the economy, similar to what the United States experienced during the 2008 Great Financial Crisis. Given the astronomical levels of debt in the Chinese economy, Beijing is desperate to avoid this scenario and will do whatever it can to subsidize domestic stakeholders, with international investors less of a priority. These actions will likely be coupled with Xi Xinping’s desire to gradually reverse some of the free-market policies initiated by Deng Xiaoping. He has made it clear that the long-term goal is not a shift towards capitalism, but back towards socialism and increased governmental control.

In recent years, China has seen a rise in geopolitical tensions with several of their neighbors and international partners, most notably in the area of trade disputes, human rights, intellectual property and the status of Hong Kong and Taiwan. These tensions have ratcheted up in recent weeks with the increased frequency of military flights near the island of Taiwan. Rolling blackouts across much of China have also led to factory shutdowns as the leadership looks to meet pollution standards ahead of key international meetings—a move that risks more disruption to global supply chains. We suspect that as tensions steadily rise, American businesses will be more deliberate in how they source products and invest in capital projects internationally. Like previous shifts in economic power, this realignment will not happen overnight, but over the course of decades, with ramifications on global partnerships and geopolitical relations. We cannot predict the outcome of these shifts; only that that they will occur. As the saying goes, change is the only constant, and the case with China is no exception.

*Preliminary results. For additional performance information, see the related GIPS® Report at the bottom of the page.

Strategy Review

The Pacific Ridge Capital Partners’ Small Cap Value strategy returned -2.4%* during the third quarter ended September 30, 2021, outperforming the Russell 2000® Value Index (“Index”) return of -3.0%. Over the trailing one-, three- and five-year periods, the strategy posted an annualized rate of return of +72.5%*, +7.6%* and +10.5%*, respectively, compared to the Index returns of +63.9%, +8.6% and +11.0%. Since inception (8/1/10), the strategy returned +11.8%* on an annualized basis, compared with +11.4% for the Index.

*Preliminary results. For additional performance information, see the related GIPS® Report on the last page.

Top Contributors and Detractors to Return for Third Quarter 2021**

Top Contributors

Rimini Street (“RMNI”) is a provider of support and services for enterprise software. The stock rebounded strongly during the third quarter after a sharp selloff in May following an earnings miss. Their quarterly results were marked by strong sales, although they had a slight miss on EBITDA. Despite strong revenue growth and improving profitability, the company continues to trade at a discount, given their long-running legal battles with Oracle. The diversification of their service offerings continues to drive their backlog and win over skeptics.

Metropolitan Bank Holding (“MCB”) is a Manhattan-based community bank. The stock rallied during the quarter as credit concerns related to the New York City economy and their health care portfolio continued to dissipate. While the company’s balance sheet has grown rapidly over the years, it has been negatively offset by steady compression in net interest margin. Management continues to seek diversification of MCB’s earnings stream though their Global Payments Group segment, adding a fintech element to the business model. In addition, a recent capital raise has provided the company with plenty of dry powder to continue to grow for the next several years.

Lifetime Brands (“LCUT”) is a manufacturer of kitchenware and tableware products. The stock rebounded strongly over the last two years after bottoming out in late 2019. Additionally, turnaround efforts by management have continued into 2021, boosted by consumer stimulus spending and new product initiatives. Recent supply chain issues and cost pressures have complicated the story somewhat, though management appears to be doing a good job of mitigating these challenges.

Stagwell (“STGW”) is a global advertising and marketing company. The stock moved higher during the quarter after the company was able to close on the acquisition of MDC Partners. (This is how we became shareholders.) Additionally, the company refinanced its entire debt balance at a more advantageous rate, adding to performance. With the combination of the two businesses, we expect STGW to gain market share in the global ad space because it can now bring a more complete offering to the table, including a mix toward digital. We are also anticipating that management will run the business more efficiently, resulting in margin expansion. While the stock has had a nice run over the past year, we still consider it to be undervalued and continue to hold it in our strategy.

ConnectOne Bancorp (“CNOB”), a New Jersey based community bank, continued its upward trajectory, enjoying a sharp recovery in its share price from the lows of 2020. The bank has consistently traded at a discounted valuation multiple as they worked through past credit issues and the difficulty of operating in a competitive market. Recent acquisitions and the resulting expense savings and improved net interest margins have helped drive profitability to new highs.

Top Detractors

Medifast (“MED”) is a direct marketer of weight loss and healthy living products. The stock gave back much of its gains from earlier in the year despite comfortably beating expectations, mostly due to disappointing guidance for the remainder of the year. The stock faced additional pressure following comments from competitors in the weight loss industry, as well as an announcement late in the quarter of competition from Amazon. The business has been growing rapidly over the past several years through increasing coach counts by 60% and productivity growth by over ten percent. Sustaining this momentum will be key to the stock recovering in the near-term.

DMC Global (“BOOM”) is a manufacturer of oil field service equipment. The stock sold off following earnings results and guidance, both of which were slightly below expectations. A combination of poor forward visibility and a capital raise during the quarter led to a dramatic 30% reduction in forward earnings estimates when compared to recent months. There is a possibility in the near future of an acquisition that will add scale and diversity to the company’s revenue streams. Additionally, the recent upward trend in oil prices should also help BOOM’s bottom line.

Healthcare Services Group (“HCSG”) is an outsourced provider of housekeeping, laundry and dietary services to long-term care and related health care facilities. The stock sold off during the third quarter for two primary reasons: The company took $10 million in reserves for legal matters related to the SEC and class action lawsuits, and a key customer had been struggling financially with the risk that it may not be paid what it is owed. In addition, labor shortages related to vaccination requirements have driven up costs in the industry. Going forward, margins should improve as occupancy trends higher and the economy slowly returns to normal.

Intevac (“IVAC”) is a manufacturer of thin film deposition used in the manufacture of hard disk drives. The stock sold off sharply during the quarter after results met expectations, but the company revised its guidance downwards. Due to reduced orders, the company pushed out key programs and may experience revenue delays on important orders because of supply chain issues. That said, a potential catalyst in the form of an investment bank hired during the quarter to explore strategic alternatives may provide a boost to performance.

Ichor Holdings (“ICHR”) is a developer and manufacturer of critical subsystems in the semiconductor capital equipment industry. The stock gave back some gains during the quarter following exceptional outperformance over the prior two years. Despite both short- and long-term demand drivers being intact, the sustained supply shortage in the industry has some investors concerned about headwinds to achieving expected operating margin expansion in the near-term.

**Past performance does not guarantee future results. The holdings identified do not represent all the securities purchased, sold or recommended to clients. Top contributors and detractors to return represent those securities that had the largest positive and negative total contribution to the overall portfolio return for the quarter. A complete list of contributors to portfolio return can be obtained by contacting Peter Trumbo, Chief Compliance Officer, at 503-886-8972 or by email at Peter.Trumbo@PacificRidgeCapital.com. For additional information, see the related GIPS® Report on the last page.

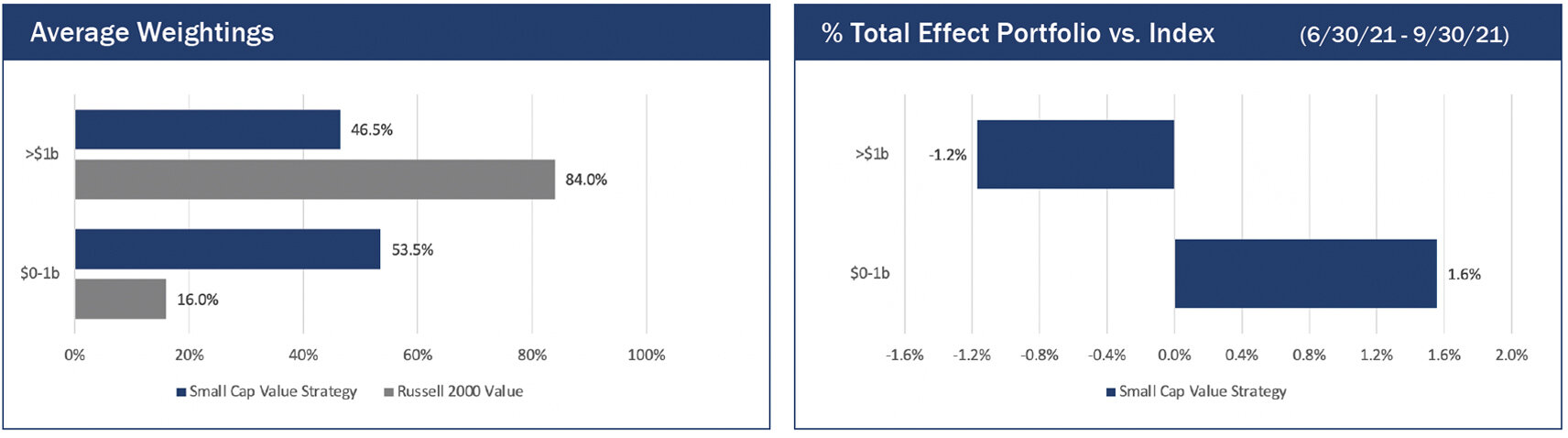

Market Capitalization Analysis

There was a slight size bias tailwind during the quarter as smaller companies in the Index outperformed larger companies. Those with a market cap under $1 billion in the Index gained 5.1%, versus a return of 4.5% for companies with a market cap above $1 billion. The strategy had 53.5% of its holdings in companies with a market cap below $1 billion, compared to 16.3% for the Index.

Style Analysis

There was a modest value-bias tailwind for profitable companies during the quarter, as stocks with lower PEs outperformed those with higher PEs. Those with a PE ratio below 15x returned +1.2% versus -3.5% for those companies with a PE greater than 15x. The strategy had 47.5% of its holdings in companies with a PE less than 15x compared to 38.6% for the Index. In addition, poor performance of unprofitable companies in the Index created a modest tailwind, as those stocks posted a -10.6% return, versus a -1.3% return for firms that were profitable. The strategy had 5.8% of its holdings in unprofitable companies, compared to 16.4% for the Index.

Economic Sector Analysis

The strategy’s performance in Financials, Communication Services, and Consumer Discretionary contributed approximately 260 basis points of excess return relative to the Index. However, performance in Industrials and Consumer Staples detracted approximately 200 basis points versus the Index. The strategy’s lack of exposure to the Utilities sector contributed approximately 10 basis points of excess return compared to the Index.

Market Outlook

We continue to look for modest growth in the US economy but are wary of hiccups in the near term caused by supply chain disruptions and a shrunken labor pool. The recovery continued at a similar pace in 2Q21 with GDP growing +6.7% driven by increased personal consumption and business re-openings. Sentiment amongst purchasing managers remains positive with the September 2021 US manufacturing PMI reading of 61.1, the 16th consecutive month of expansion. New Orders and Production components remain strong while inventories appear to be building slightly. However, transportation bottlenecks have significantly stalled the pace of deliveries setting up a potential restocking event into next year as the flow of goods improves.

Portfolio Characteristics and Top Ten Holdings (as of 9/30/21)

As always, we continue to search for companies that demonstrate an ability to earn a fair return on capital. We welcome any questions or comments you may have and thank you for your continued support.

Sincerely,

Pacific Ridge Capital Partners

Investment Team Additional Professionals

Mark Cooper, CFA® Co-Senior Portfolio Manager Peter Trumbo Chief Operating/Compliance Officer

Dominic Marshall, CFA® Co-Senior Portfolio Manager Mike McDougall Senior Trader

Ryan Curdy, CFA® Portfolio Manager Manisha Thakkar, CFA® Director of Business Development

Justin McKillip, CFA® Senior Analyst Veronica Orazio Operations Assistant

Adam Boyce, CFA® Senior Analyst

Regulatory Disclosures

The contributors and detractors to return, market capitalization weightings and total effect, economic sector weightings and total effect, portfolio characteristics, and top ten holdings for the Small Cap Value Composite are based on a representative account within the strategy. The representative account statistics are shown as supplemental information and complement the composite's GIPS® Report as provided on the last page.

The Russell 2000® Value Index measures the performance of the Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. For comparison purposes, the Index is fully invested, which includes the reinvestment of income. The return for the Index does not include any transaction costs, management fees or other costs.

In order to maintain consistency when comparing the Small Cap Value strategy to the Russell benchmark, the Firm utilizes FactSet’s outlier methodology calculations which provide a comparable portfolio characteristic calculation methodology as Russell applies to its indices.

The information provided should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in our strategy at the time you receive this report or that securities sold have not been repurchased. It should not be assumed that any of the holdings discussed herein were or will be profitable or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. Past performance is no guarantee of future results.

Although the statements of fact and data in this report have been obtained from, and are based upon, sources that the Firm believes to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed. All opinions included in this report constitute the Firm’s judgment as of the date of this report and are subject to change without notice. This report is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security.

PRCP GIPS Report

Disclosures

Pacific Ridge Capital Partners, LLC (“Pacific Ridge”, “PRCP”, or “the Firm”) is a 100% employee owned investment advisor registered with the Securities and Exchange Commission under the Investment Advisors Act of 1940. The Firm was established in June 2010, and has one office located in Lake Oswego, Oregon. Pacific Ridge claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Pacific Ridge has been independently verified for the periods June 10, 2010 through September 30, 2021. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. The Small Cap Value Composite has had a performance examination for the periods June 10, 2010 through September 30, 2021. The verification and performance examination reports are available upon request.

The Small Cap Value composite was created and incepted on August 1, 2010. The Small Cap Value composite comprises fully discretionary portfolios managed by the Firm invested primarily in an equity portfolio of small companies with market capitalizations similar to those found in the bottom three-quarters of the Russell 2000® Index. The strategy ascribes to a disciplined bottom-up fundamental selection process with an emphasis given to the cash flow generating capabilities of a company. The strategy’s objective is to outperform the Russell 2000® Value Index which is used as our benchmark. Eligible portfolios must be managed for a full calendar month prior to inclusion in the Small Cap Value composite. Composite dispersion is measured using an asset weighted standard deviation of gross returns of the portfolios included for the entire year. Returns and asset values are stated in US dollars.

The Russell 2000® Value Index measures the performance of the Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. For comparison purposes, the index is fully invested, which includes the reinvestment of income. The return for the index does not include any transaction costs, management fees or other costs.

Sources: Pacific Ridge; FactSet Research Systems (“FactSet”); and Russell Investment Group (“Russell”) who is the source and owner of the Russell Index data.

Returns for the Small Cap Value composite are presented gross and net of management fees and other expenses and includes realized and unrealized gains and losses, cash and cash equivalents and related interest income, and accrued based dividends. Net returns are calculated by deducting the highest annual management fee of 1.00% from the quarterly gross composite return. Performance-based fees are available upon request. All returns are calculated after the deduction of the actual trading expenses incurred during the period. The management fee schedule and total expense ratio for the Small Cap Value Fund, which is included in the composite, are 1.00% on all assets and 1.23%, respectively, as of the most recent audit. Total fees for the fund may not exceed 1.25% annually.

The fee schedule for separately managed accounts is a flat rate of 1.00%.

The portfolio characteristics, sector weightings and attribution analysis for the Small Cap Value composite are based on a representative account within the strategy. The representative account statistics are shown as supplemental information. The Firm maintains a complete list and description of composites and pooled funds, policies for valuing portfolios, calculating performance, and preparing GIPS Reports which are available upon request by contacting Peter Trumbo, Chief Compliance Officer at (503) 886-8972 or Peter.Trumbo@PacificRidgeCapital.com.

GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

Top 5 and Bottom 5 Performing Securities represent those security holdings that had the largest positive and negative total contribution to the portfolio return. Top 3 and Bottom 3 Economic Sectors represent those sectors that had the largest positive and negative total contribution to the portfolio return.

In order to maintain consistency when comparing the Small Cap Value strategy to the Russell benchmark, the Firm utilizes FactSet’s outlier methodology calculations which provide a comparable portfolio characteristic calculation methodology as Russell applies to its indices.

The information provided should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in our strategy at the time you receive this report or that securities sold have not been repurchased. It should not be assumed that any of the holdings discussed herein were or will be profitable or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. Past performance is no guarantee of future results.

Although the statements of fact and data in this report have been obtained from, and are based upon, sources that the Firm believes to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed. All opinions included in this report constitute the Firm’s judgment as of the date of this report and are subject to change without notice. This report is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security.