Investment Philosophy

Pacific Ridge Capital Partners ("PRCP") is excited to be nearing its one-year anniversary and we have enjoyed meeting with many of you during that time. As we have shared, this new firm fits like an old glove. The team is happy to be back together in an employee-owned structure, with a time-tested investment philosophy and process. This new start has also given us an opportunity to update the presentation of our investment philosophy and core beliefs.

Down below, you'll find the Pacific Ridge Capital Partners Value Zone™. This graph is a simple illustration of the basic premise of our philosophy: buy low-expectation stocks with significant upside, based on long-term, valuation-focused research.

The three companies (A, B, and C) represented on the graph have a Return on Equity (ROE) of 10%. Yet the price that the market is willing to pay for each company is wildly different. On the vertical axis, we have the Price-to-Book multiple for each company. Along the horizontal axis, we have the ROE that each company generates. The Red Line represents a market return of 10%. For example, point B represents a company that currently has a ROE of 10%. If you, as an investor, want a 10% return, you would pay a multiple of 1x for that company's equity. However, if you wanted a return of 20%, you would only pay 0.5x book value – point C. If you were willing to accept only a 5% return, then you would pay 1.5x book value – point A.

Even the casual observer would quickly point out that all three companies generate the same exact ROE, so why would anyone pay a different price for each company? The answer is that you expect something different from each company in the future. Company A has very high expectations, and Company C has very low expectations. We like to look for companies where we think other investors are wrong in their assessment – those companies below the line. This allows us to buy very good companies at very low prices.

Of course, we are not the only team to employ this value/ contrarian approach to investing. For example, Charles Ellis's "Winning the Loser's Game" highlights this core fundament belief of ours: buying low expectations and avoiding potential big losses is the easiest way to stack the deck in our clients' favor. Our proven track record of following this approach, and marrying it with indepth research done by an experienced team makes for differentiated offerings in the form of our PRCP Small Cap Value and Micro Cap Value strategies. Avoiding big losses and looking for stocks that we expect can double over our typical five-year investment horizon has served our clients well.

If you are amongst those who have met with us over the past year, you have probably heard us say that you can expect three consistent biases from PRCP as an investment manager:

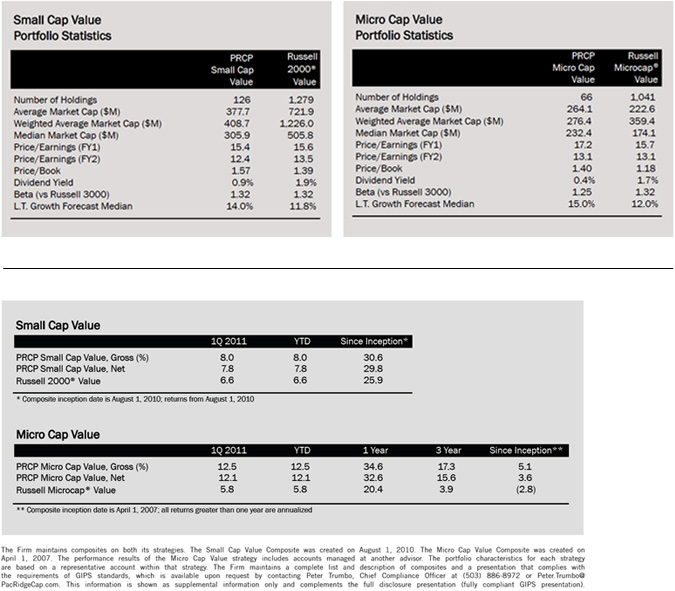

SIZE – Our Small Cap and Micro Cap strategies look for companies in the sub-$500 million market cap range for new purchases. This is the domain of inefficientlypriced opportunities. These smaller companies represent private equity upside with public equity liquidity.

VALUE – We live, eat and breathe in the PRCP "Value Zone." We will elaborate on each of the primary characteristics in stocks that we pursue in our coming quarterly letters. But we believe that it is foundational to take a long-term, patient, and diligent approach in our process. The market's short-term mindedness, fickleness, and neglect create significant opportunities for us.

SECTORS – We do not try to mimic the index benchmarks in any way from a sector or industry perspective. To do so might be perceived by some as "safe," but we believe in taking the best opportunities the market is giving us and letting the sector and industry weightings fall as they may. This has served us well, allowing us to construct our strategies from a bottom-up, stockpicking perspective, with the best-of-the-best long-term opportunities.

During the coming year, we will continue to search for companies that demonstrate an ability to earn a fair return on capital. As always, we welcome any questions or comments you may have. Thank you for your continued support.

Sincerely,

Pacific Ridge Capital Partners

About Pacific Ridge Capital Partners

Pacific Ridge Capital Partners is an employee-owned firm. We generate our own investment ideas using fundamental analysis and bottom-up stock picking. The investment team applies a consistent, patient and disciplined process that results in low turnover and stability. Our proven philosophy has performed well over many investment cycles and it is the consistent application of this strategy that makes Pacific Ridge unique.

The principals of Pacific Ridge Capital Partners are invested along with our clients in each of our strategies.

PRCP Small Cap Value – Our Small Cap Value strategy generally purchases stocks in the bottom three-quarters of the Russell 2000® Index. This smaller capitalization segment has a large number of underfollowed companies, providing us the greatest opportunity to exploit market inefficiencies. The typical range of holdings is between 100 and 150.

PRCP Micro Cap Value – Our Micro Cap Value strategy generally purchases stocks in the Russell Microcap® Index. This segment is widely underfollowed, providing us the greatest opportunity to exploit market inefficiencies. The typical range of holdings is between 50 and 80.

We believe these market cap segments offer great potential returns and additional diversification for our clients. For further information about Pacific Ridge Capital Partners and our investment strat- egies, we invite you to contact Tammy Wood via email at Tammy.Wood@PacificRidgeCapital.com or by phone at (503) 878-8502.

Disclosures

Pacific Ridge Capital Partners, LLC (“Pacific Ridge”, “PRCP”, or “the Firm”) is an employee-owned investment advisor registered with the Securities and Exchange Commission under the Investment Advisor Act of 1940. The Firm was established in June 2010, and has one office located in Lake Oswego, Oregon. Pacific Ridge claims compliance with the Global Investment Performance Standards (GIPS®).

Sources: Pacific Ridge; FactSet Research Systems (“FactSet”); and Russell Investment Group (“Russell”) who is the source and owner of the Russell Index data.

The current annual investment advisory fees for the portfolios managed in the Firm’s Small and Micro Cap Value strategies are 1.00% and 1.50% of assets, respectively. Returns for the composites are presented gross and net of management fees and other expenses and includes realized and unrealized gains and losses, cash and cash equivalents and related interest income, and accrued based dividends. The Firm calculates time weighted rates of return by geometrically linking portfolio simple rates of return at least monthly, with adjustments made for significant external cash flows. The composite returns are calculated by asset weighting the individual portfolio returns using beginning of the period values. All returns are calculated after the deduction of the actual trading expenses incurred during the period.

The information provided should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in our strategy at the time you receive this report or that securities sold have not been repurchased. It should not be assumed that any of the holdings discussed herein were or will be profitable or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. Past performance is no guarantee of future results.

Although the statements of fact and data in this report have been obtained from, and are based upon, sources that the Firm believes to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed. All opinions included in this report constitute the Firm’s judgment as of the date of this report and are subject to change without notice. This report is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security.

The Russell 2000® Value Index measures the performance of the Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. For comparison purposes, the index is fully invested, which includes the reinvestment of income. The return for the index does not include any transaction costs, management fees or other costs.

The Russell Microcap® Value Index measures the performance of the microcap segment of the U.S. equity market. For comparison purposes, the index is fully invested, which includes the reinvestment of income. The return for the index does not include any transaction costs, management fees or other costs.

Returns and asset values are stated in US dollars.